by William J. Moser.

In this manuscript, I examine the firm’s ex ante cost of equity capital in the quarter before and the quarter after the filing of a shareholder securities lawsuit as well as in the quarter before and the quarter after the final resolution of the shareholder lawsuit.

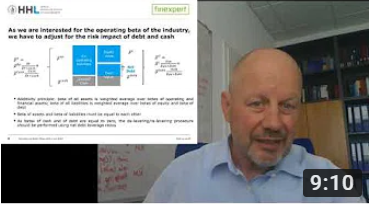

Tackling practical questions of financial analysts and providing some guidance to answer them for your day to day business..

Tackling practical questions of financial analysts and providing some guidance to answer them for your day to day business..